Small charges have a way of piling up quietly. A streaming service here, a rate increase there—before you know it, your monthly bills have crept up by hundreds of dollars without any real change in what you're getting.

The good news is that most of these expenses are negotiable, switchable, or simply unnecessary. This guide walks through 15 practical ways to cut your recurring costs, from cell phone plans and insurance to subscriptions you forgot you had.

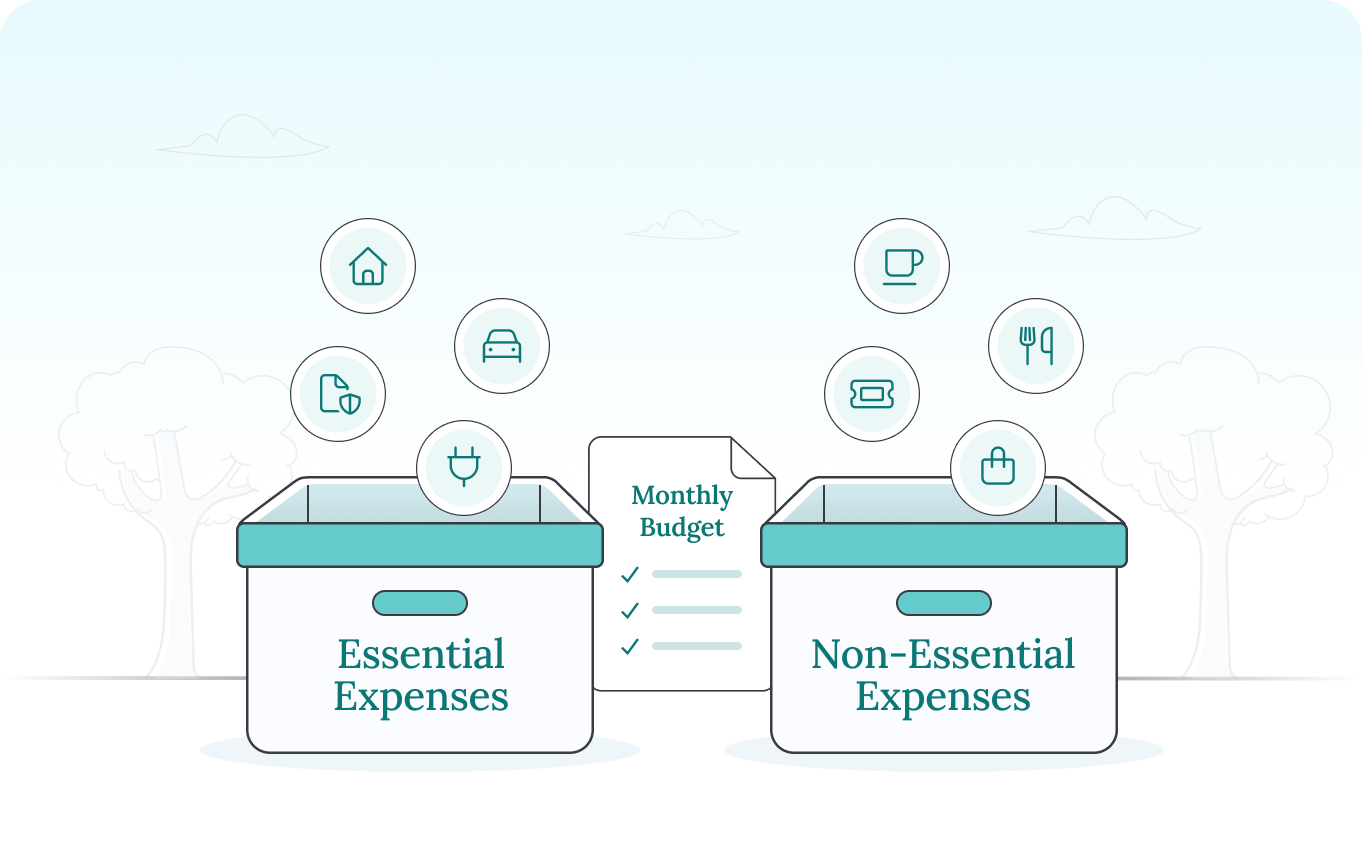

Where is your money going each month

Reducing monthly expenses starts with tracking where your money actually goes. Pull up your bank and credit card statements from the past two or three months and look for every recurring charge. Most people find subscriptions they forgot about or services they barely use.

Once you see the full picture, you can tackle each category one at a time. Here are the most common monthly bills to look for:

- Housing: rent or mortgage payments

- Utilities: electricity, gas, water, trash

- Insurance: car, home, renters

- Telecom: cell phone, home internet

- Subscriptions: streaming, apps, gym memberships

- Loans: car payments, student loans, credit cards

How to cut your cell phone bill

Cell phone plans are one of the easiest places to find savings. Most people pay for far more data than they actually use each month, and wireless carriers count on that.

Switch to a lower cost carrier

Budget carriers like Mint Mobile, Visible, or Cricket use the same networks as major providers. The coverage is often identical, but the monthly cost can be significantly lower.

Downgrade your data plan

Check your phone settings to see how much data you actually use. If you're consistently under your limit, a smaller plan could save you $20 or more each month.

Remove unused lines or features

Look at add-ons like device protection, international calling, or extra lines for family members who no longer live with you. Small charges add up quietly over time.

How to lower your car insurance costs

Car insurance rates vary widely between providers, yet most people stick with the same company for years without comparing. Shopping around is one of the most effective ways to lower this recurring expense.

Shop around and compare quotes

Getting quotes from at least three different insurers can reveal significant price differences for the same coverage. Platforms like Wisepal can automate this comparison for you.

Raise your deductible

Your deductible is the amount you pay out of pocket before insurance kicks in. Choosing a higher deductible typically lowers your monthly premium. Just make sure you could cover that amount if you needed to file a claim.

Ask about discounts you qualify for

Many discounts go unclaimed simply because people don't ask. Common ones include:

- Safe driver discount: for accident-free records

- Bundling discount: for combining home and auto policies

- Low mileage discount: for driving under a certain number of miles annually

- Good student discount: for young drivers with strong grades

How to reduce your home internet bill

Internet service is another area where most households overpay. Many regions have limited provider options, but you still have more leverage than you might think.

Negotiate with your current provider

Call your provider and ask if any promotional rates are available. Mentioning that you're considering switching to a competitor often unlocks discounts that aren't advertised. Retention departments typically have more flexibility than regular customer service.

Switch to a cheaper plan or provider

Many people pay for speeds they don't actually use. If you're not streaming on multiple devices at once or gaming competitively, a mid-tier plan usually works fine.

Return rental equipment and buy your own

That $10-15 monthly modem rental fee adds up to over $150 a year. Buying your own compatible modem and router typically pays for itself within six to eight months.

How to save on electricity and utility bills

Utility bills fluctuate with the seasons, but small adjustments can reduce your baseline costs throughout the year.

Adjust your thermostat settings

Lowering your thermostat by just two degrees in winter or raising it in summer can cut heating and cooling costs noticeably. A programmable or smart thermostat makes this automatic when you're asleep or away.

Upgrade to energy efficient appliances

When it's time to replace an old appliance, choosing an Energy Star-rated model can lower your electricity usage. The upfront cost is often offset by monthly savings within a year or two.

Compare electricity providers in deregulated markets

If you live in a state with energy choice, like Texas, Ohio, or Pennsylvania, you can shop for electricity suppliers the same way you'd compare cell phone plans. Rates can vary by several cents per kilowatt-hour, which adds up quickly.

How to lower your home insurance premium

Home insurance is easy to set and forget, but rates often creep up annually without any change in your coverage. A quick review can reveal opportunities to pay less.

Increase your deductible

Similar to car insurance, raising your home insurance deductible can reduce your premium. This trade-off works well if you have an emergency fund to cover smaller claims.

Bundle home and auto policies

Most insurers offer multi-policy discounts when you combine home and auto coverage. The savings typically range from 5% to 25% depending on the company.

Review coverage limits annually

Your coverage limits might not match your current situation. If your home's value has changed or you've sold expensive items, adjusting your policy could lower your costs.

How to refinance your car loan for a lower payment

Refinancing means replacing your current loan with a new one at better terms. If interest rates have dropped since you bought your car, or if your credit score has improved, refinancing could lower your monthly payment.

This option works best when you have at least a year or two left on your loan and can qualify for a rate at least one percentage point lower than your current one.

How to negotiate with service providers

Negotiation is an underused approach for cutting monthly expenses. Many providers would rather give you a discount than lose you as a customer.

Know your current rate and competitor offers

Before calling, research what competitors charge for similar service. Having specific numbers ready strengthens your position.

Ask for loyalty or retention discounts

When you call, ask to speak with the retention department. These teams often have access to unadvertised discounts designed to keep customers from leaving.

Be ready to switch if they refuse

Your leverage comes from your willingness to actually leave. If a provider won't budge, following through on switching sends a message. You might even get a callback with a better offer.

How to cancel unused subscriptions and memberships

Small recurring charges are easy to overlook, yet they can add up to hundreds of dollars annually. A streaming service here, a forgotten app there—it accumulates faster than most people realize.

Audit your bank and credit card statements

Go through your statements line by line and flag every subscription. Ask yourself: when did I last use this? If the answer is more than a month ago, it might be time to cancel.

Use a subscription tracking tool

Platforms like Wisepal can automatically detect recurring charges across your accounts, making it easier to spot subscriptions you've forgotten about.

Set reminders before free trials end

Free trials that convert to paid subscriptions are a common source of unwanted charges. Setting a calendar reminder a day or two before the trial ends gives you time to decide whether to keep it.

How to use autopay discounts to reduce bills

Many service providers offer small discounts for enrolling in automatic payments. While each discount seems minor, they add up across multiple bills.

Common bills that offer autopay discounts include car insurance, cell phone plans, internet service, and some utility providers.

How to bundle services for extra savings

Bundling combines multiple services with one provider in exchange for a discount. Common bundles include home and auto insurance or internet and phone service.

One caution: always compare the bundled price against what you'd pay for separate providers. Sometimes the "discount" still costs more than mixing and matching.

How to review your bills regularly for rate increases

Providers often raise rates quietly after promotional periods end. What started as a great deal can gradually become overpriced without you noticing.

Setting a quarterly reminder to review your recurring bills helps catch rate increases early. Wisepal can also monitor your bills automatically and alert you when rates change.

How to compare providers without losing key benefits

One common fear about switching is losing coverage or features you depend on. The key is making an apples-to-apples comparison before you commit.

Wisepal scans your current plan's terms and finds alternatives that match your existing benefits at a lower price, so you're not sacrificing coverage for savings.

Tools and apps that help lower monthly bills

Several categories of tools can help you reduce expenses, each with a different approach.

Bill negotiation services

Bill negotiation companies call providers on your behalf to negotiate lower rates. They typically charge a percentage of your savings.

Subscription management apps

Subscription trackers monitor recurring charges and help you cancel unused subscriptions with a few taps.

Comparison and switching platforms

Comparison platforms find better rates across multiple bill categories and help you switch seamlessly. Wisepal falls into this category. It's free, covers multiple bill types, and handles the switching process for you.

Take control of your monthly expenses and start saving

Lowering your monthly bills doesn't require hours of research or uncomfortable phone calls. By working through each category systematically, you can often find meaningful savings.

Pick one bill from this list and take action on it this week. Small wins build momentum, and before long, you'll have more money staying in your pocket each month.