Personal finance is the practice of managing your money through budgeting, saving, spending, investing, and protection—basically, every decision you make about what to do with your paycheck and beyond. It sounds straightforward, but most people never learned this stuff in school and end up figuring it out through trial and error (often expensive error).

This guide covers the five core areas of personal finance, practical tips for beginners, and simple ways to reduce your monthly bills without spending hours on research.

What is personal finance

Personal finance is the practice of managing your money through budgeting, saving, spending, investing, and protecting your assets. It covers every decision you make about earning, spending, and growing your money, from choosing a cell phone plan to planning for retirement. Put simply, personal finance is what you choose to do with your money.

Five core areas make up personal finance:

- Income: What you earn from work, investments, or other sources

- Spending: What goes out each month on bills, purchases, and daily expenses

- Saving: What you set aside for short-term goals and emergencies

- Investing: What you grow over time through retirement accounts or other assets

- Protection: What you insure against unexpected losses

Each area connects to the others. Reducing your spending frees up more money for saving. Saving consistently allows you to invest over time. And protecting your income with insurance keeps the rest of your plan intact when something goes wrong.

Why personal financial management matters

Good personal money management helps you avoid living paycheck to paycheck, handle emergencies without panic, and build toward the things you actually want. Without a plan, it's easy to overspend without realizing it and then wonder where your money went at the end of each month.

Here's what solid financial management can do:

- Financial stability: You can cover unexpected expenses like car repairs or medical bills without going into debt.

- Less stress: Knowing where your money goes each month removes a lot of anxiety around finances.

- Future security: You build wealth over time instead of just getting by.

The good news? You don't have to become a financial expert to see real improvements. Even small, consistent steps add up.

Five personal finance basics everyone should know

The following five areas form the foundation of basic personal finance. They apply to everyone, regardless of income level.

1. Make a monthly budget that works for you

Budgeting is tracking your income versus your expenses. It shows where your money actually goes, not where you think it goes.

A popular starting point is the 50/30/20 rule. This framework divides your after-tax income into three categories: 50% for needs like housing, groceries, and utilities; 30% for wants like dining out and entertainment; and 20% for savings and debt payoff.

You might find those percentages don't fit your situation perfectly, and that's fine. The point is to have a framework that helps you spend intentionally rather than reactively. Even a rough budget beats no budget at all.

2. Build an emergency fund before anything else

An emergency fund is savings set aside specifically for unexpected costs. Job loss, medical bills, car repairs, a broken appliance—life has a way of throwing surprises at you.

Financial experts typically recommend saving three to six months of living expenses, though even $1,000 is a meaningful start. Why prioritize an emergency fund before investing? Because without one, any surprise expense can push you into high-interest debt, which undoes your progress elsewhere.

Think of an emergency fund as the foundation that keeps the rest of your financial plan stable.

3. Pay off debt and avoid taking on more

Not all debt is created equal. A mortgage or student loan can be considered "good debt" because it often comes with lower interest rates and builds toward something valuable. High-interest credit card debt, on the other hand, can spiral quickly and eat into your income.

If you're carrying multiple debts, two common approaches can help:

- Avalanche method: Pay off the highest-interest debt first to minimize total interest paid over time.

- Snowball method: Pay off the smallest balance first for quick wins and motivation.

Either way, the goal is to stop losing money to interest so you can redirect those payments toward saving and investing.

4. Start saving and investing for your future

Investing is how you grow wealth over time, and it's more accessible than many people realize. Retirement accounts like a 401(k) or IRA offer tax advantages that make your money work harder.

The key concept here is compound interest. When your money earns returns, and then those returns earn returns, growth accelerates over time. Starting early matters more than starting big. Even modest contributions in your twenties can outpace larger contributions made later, simply because of the extra time for compounding.

If your employer offers a 401(k) match, that's essentially free money. Contributing enough to get the full match is one of the simplest financial wins available.

5. Get the right insurance to protect your income

Protection is the often-overlooked pillar of personal finances. Insurance—health, auto, home or renters, and life—protects everything else you've built. Without it, a single accident or illness can wipe out years of savings.

The right coverage depends on your situation. However, reviewing your policies periodically ensures you're not underinsured or overpaying for coverage you don't actually use. Many people sign up for a policy and never look at it again, even as their circumstances change.

Personal finance tips for beginners

Once you understand the basics, a few practical habits can make managing your money feel less overwhelming.

Automate your savings and bill payments

Setting up automatic transfers to your savings account removes the temptation to skip saving "just this month." Similarly, enabling autopay for bills helps you avoid late fees and keeps your credit score healthy.

Automation works because it takes willpower out of the equation. You save first, then spend what's left, rather than hoping there's something left to save. Most banks and employers make this easy to set up.

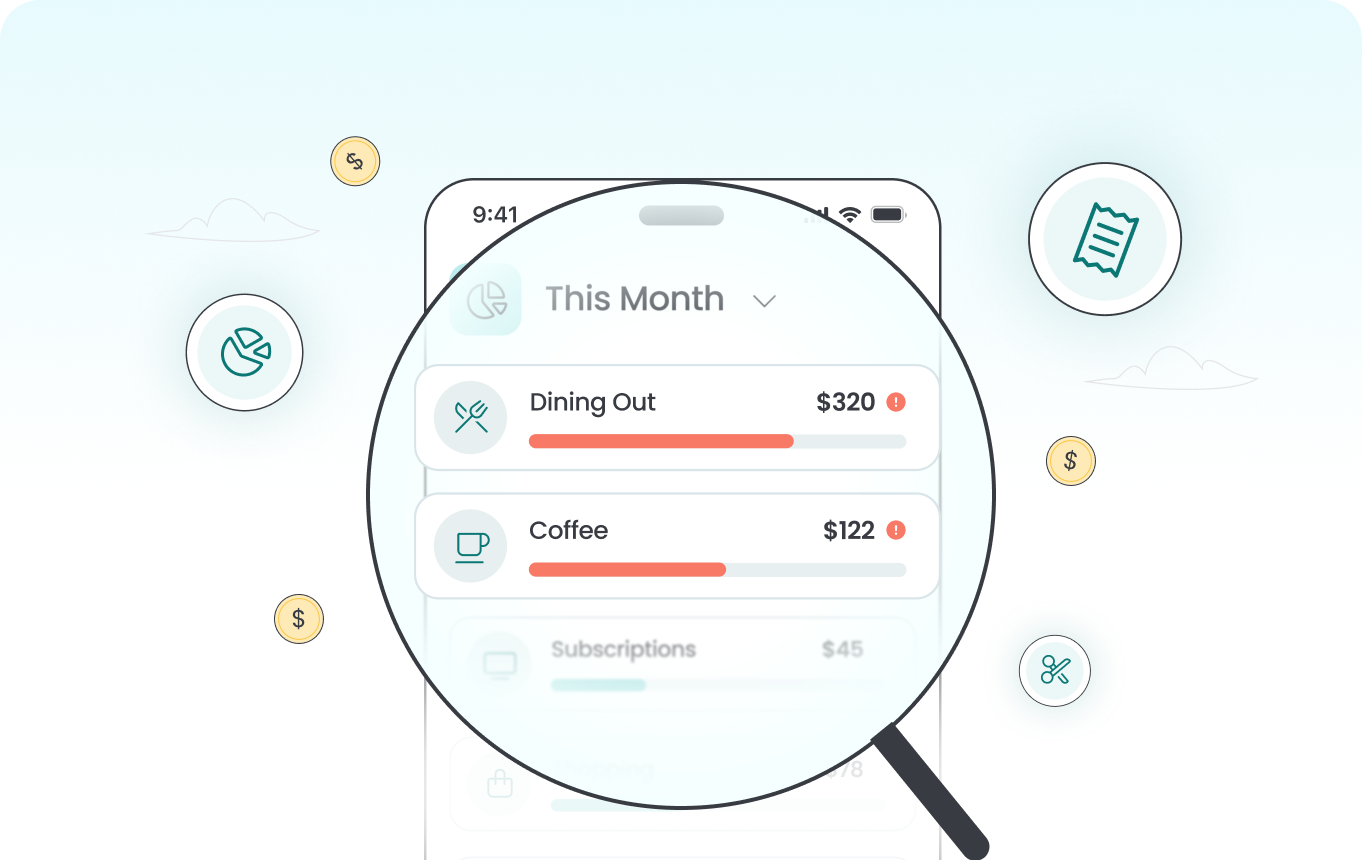

Review your recurring bills at least once a year

Many people set and forget subscriptions, insurance policies, and service plans. Over time, rates creep up or better options become available, and you end up overpaying without realizing it.

An annual "bill audit" is one of the simplest ways to find extra money in your budget. Look at your cell phone plan, internet service, insurance premiums, and streaming subscriptions. Are you still using everything you're paying for? Are there better rates available?

Even 15 minutes of review can reveal savings you didn't know existed.

Use a tool that finds savings for you

Managing personal finance doesn't have to mean hours of research. Platforms like Wisepal can scan your bills and find better rates automatically, for free. This is especially helpful if you suspect you're overpaying but don't have time to compare every provider yourself.

The idea is simple: instead of manually researching alternatives for each bill, a tool does the comparison work and shows you where you can pay less for the same coverage or service.

How to reduce your monthly expenses without hours of research

This is where personal money management advice gets practical. You can often lower your bills without changing your lifestyle, just by switching to better options.

Lower your cell phone and internet bills

Cell phone and internet plans are common areas where people overpay. Carriers frequently offer promotional rates to new customers while existing customers stay on older, pricier plans.

Comparing options can reveal savings of $50 or more per month without sacrificing coverage or speed. If you've been with the same provider for a few years, it's worth checking what else is available.

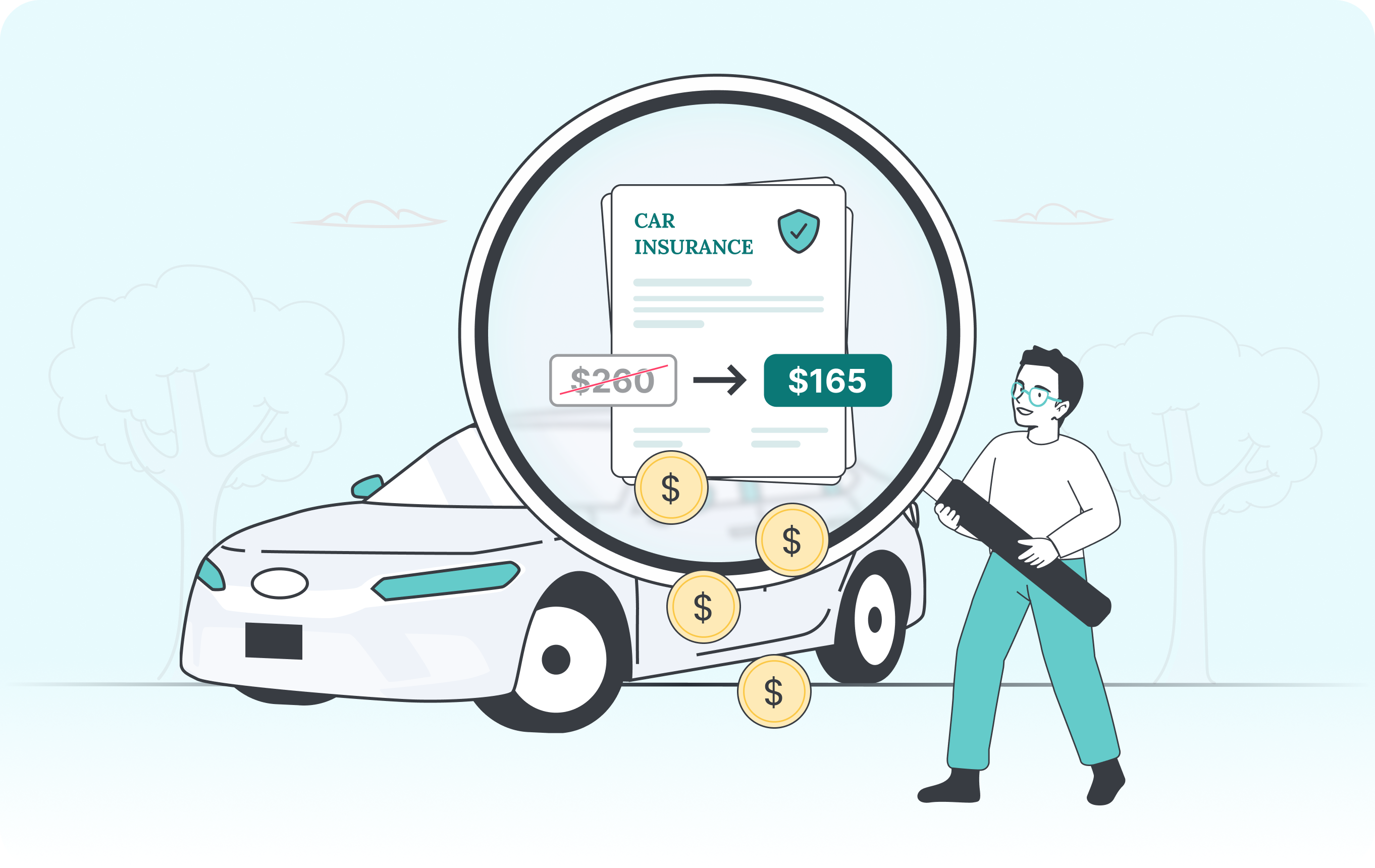

Find cheaper car insurance and home insurance

Insurance rates vary widely between providers for the same coverage. What you paid when you first signed up may no longer be competitive, especially if your circumstances have changed.

Getting quotes from multiple providers every year or two is one of the highest-impact moves in personal financial management. Many people find significant savings just by switching, without reducing their coverage.

Switch to better credit cards or loans

Higher-yield savings accounts and lower-interest loans can make a meaningful difference over time. If your savings account earns 0.01% while others offer 4% or more, you're leaving money on the table.

Similarly, refinancing a car loan or consolidating credit card debt at a lower rate reduces how much you pay in interest. That frees up money for other goals.

Cut utility costs without changing your habits

In areas with deregulated electricity markets, you can often choose your provider. Switching to a different plan or provider can lower your bill without requiring any lifestyle changes.

Tip: If comparing all your bills feels overwhelming, Wisepal can check for savings across multiple categories at once, so you can see where you're overpaying without doing the research yourself.

Personal finance mistakes that keep you overpaying

Even people who understand the basics sometimes fall into patterns that cost them money. A few common ones:

- Never comparing bills: Sticking with the same provider for years without checking alternatives often means paying more than necessary.

- Ignoring subscriptions: Paying for services you forgot you signed up for adds up quickly.

- Choosing convenience over value: Accepting default plans instead of shopping around usually benefits the provider, not you.

- Waiting too long to start: Delaying saving and investing because it feels complicated costs you the most valuable asset, which is time.

Recognizing these patterns is the first step toward breaking them.

Simple personal money management starts here

Personal finance for beginners doesn't have to be overwhelming. Small steps like budgeting, automating savings, and reviewing bills add up over time and create real momentum.

If you're looking for a place to start, checking your recurring bills is one of the fastest ways to find extra money in your budget. Wisepal can help you find savings automatically, for free, so you can improve your finances today without the hassle.